Operation Saylor - Episode 27/120

Hi again and welcome to another episode of the Operation Saylor. This is update number 27, corresponding to September 2024.

If you are reading this for first time, you might want to check Episode 1, where my plan and details are explained. That will get you in context.

Stats

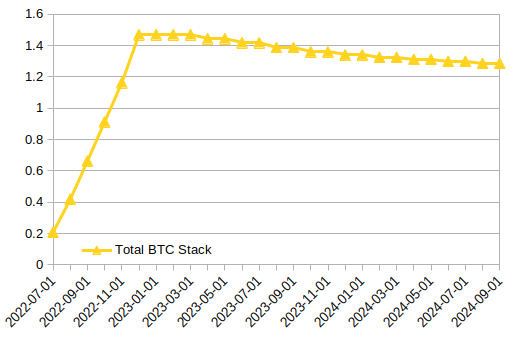

- BTC stack: 1.28537210BTC

- € stack: 128.80 €

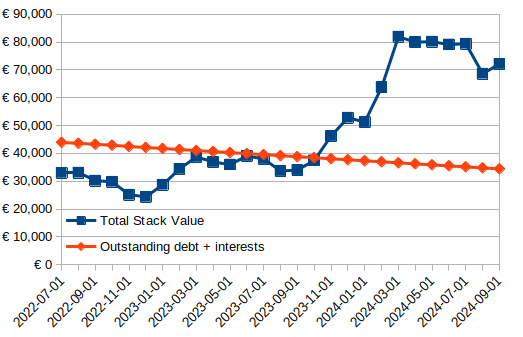

- Current total value in €: 72,109.64 €

- € into BTC: 30,000 €

- Paid back to bank: 9,521.20 €

- Outstanding debt + interests: 34,423.13 €

- Installments to go: 94

Charts

Log

Hello again and welcome to another episode of the series. This month, I've prepared a bit of an off-topic-ish rant on insurance and how Bitcoin has changed my relationship with them.

Stories

Let me begin with three tiny stories.

First one: recently, a friend of mine who runs a brick and mortar business had some water leakage problems at his shop. He's not the owner of the space, he's renting. As per his rental agreement, it's the landlord who is responsible for taking care of this kind of stuff, so he got in touch. The landlord didn't raise any issues: he has an insurance for the shop space, so he just got in touch with the insurance company and once the claim was open, got my friend in the loop so he could take care of the logistics, which makes all the sense since my friend could better manage that to minimize disruption in his business.

What came after was a complete mess up. The insurance company seemed to respond promptly, but they just kept on sending clueless guys who would just take a look at the damaged stuff, make some silly guess on what was the root cause and attempted some half-assed approach to solving it. The fixes would never work for more than a couple of weeks, which led to my friend getting in touch again, and the insurance company sending off again a different guy, who still was clueless, and who obviously got absolutely no kind of handover from the previous guy. The new guys would proceed again to do his part, screw up, and fly off. This cycle repeated itself four times with four different handymen.

Finally, my friend, who at this stage was pretty close to throwing someone off a window, decided to call a handyman he trusted from years ago, unrelated to the business. Pretty frustrating, since it was the landlord's and his insurance responsibility, but the issue was disrupting his business operation enough that he was better off going down this path. The trusted handyman permanently fixed the issue in a single visit and charged only 250€.

Second one: a couple I'm friends with got pregnant a few months ago. They live in the UK. With the NHS being in shambles, they decided to manage the whole pregnancy through her private health insurance. They started with the first visits and everything was smooth and fine, until time came to run some tests to spot genetic issues in the baby, such as Down's syndrome. Low and behold, their doctor pointed out that there were multiple pretty good tests for that kind of issues, but that the insurance company wouldn't pay for them. Confused, since the couple thought everything related to the pregnancy would be included, the couple went back to the insurance terms and read the fine print. They found that the terms pretty much stated that everything and all tests were included, EXCEPT for these ones being discussed specifically. In the end, they just had to accept the terms and ended up paying that out of their pocket, which they told me cost a bit less than a 1000 pounds.

Third one: a relative of mine went on holiday to Greece this summer. Her and her direct family planned a roadtrip, so they rented a car in Athens from one of the typical big name companies you find at every airport. My relative, being as risk averse as you could imagine, went straight for the premium insurance that she got offered.

Unfortunately, they did have an accident a few days later. Luckily it was a minor crash in terms of personal damages for them, but on of the front corners of the car got pretty busted (they had to get a replacement car from the company since the one they had wasn't driveable after the impact). Towards the end of the trip, when they got back to the original office where they started the rental, the company workers informed that the insurance they had purchased didn't cover the damages on the rim and wheel that were hit. My relative got angry as fuck, because the wording of the insurance package was pure trickery to get you convinced it covered anything and everything. But just like with the previous couple insurance terms, the terms did state that wheel and rim damages weren't covered, so my relative had to pay up for that.

The decision

I guess the point I'm heading to is pretty clear: insurance services of all sorts fucking suck.

But besides the frustration and anger caused by shitty service, absurd fine prints and nasty trickery, I've been pondering for some time already on a more level-headed question: are they economically worth it? Which ties very directly with the obvious decision to be made: should I purchase them?

To answer this, I had to structure my thoughts a bit.

Let's start from the simplest model ever. Let's suppose we are judging purchasing insurance for whatver thingy for some period of time. The most naive model I can thing of is:

- Compute how much you'll pay in premiums (insurance cost)

- Multiply the chances of the insurable bad event happening times the expected cost of it (bad event cost)

- The insurance makes sense if:

- Bad event cost is higher than insurance cost

- Or bad event cost is higher than all your savings and accessible debt, which means facing it could wreck your life

That all probably sounds reasonable, but life isn't that simple. Let me detour with some reflections.

Types of insurance and game theory

The first I did was to make a bit of a taxonomy, because insurance is used to describe a gazillion different types of trades.

First, the common point to all of them is that you are offloading risk: there's some bad event which might or might not happen, and which will have bad consequences of some type for you if it does happen. So, you pay a company so they shift the risk onto themselves, and in turn they will help you out in some way if the bad thing does happen. Otherwise, they just keep your money.

But from that common ground, there are several branches. I'll split things by two dimensions. The first dimension is whether the help from the insurance company in case of the negative event is money, or having your problem solved. Examples for the first are life and disability insurances, or a theft insurance for a vehicle where the insurance company will pay you money, not get you another vehicle. Examples for the second are health insurance or a home insurance, where the company will hire people to help you out.

The other dimension is the monetary sizing of the bad event. There are insurances, like a home insurance or that car rental insurance from my relative, that frequently deal with rather small damages and issues. Stuff that has costs around 2, 3, maybe 4 digits worth of bucks. Other insurances agreements cover events that are big bucks, such as life insurance or a third party liability car insurance, which might pay hundreds of thousands or even millions under certain circumstances.

With those types and categories in mind, here's my two cents on practical game theory around the different combinations.

First of, common ground for all insurances: the insurance company is incentivised to cash in your premiums, and bleed out as little as possible, as late as possible, let it be in helping you out, paying you out, or dealing with your complaints or lawsuits. I would imagine some small insurances, somewhere, at some point in history, must have been run in an honest way and truly placed the well-being of customers in a pedestal. But for the modern, large corporations versions I see in my life, I'm pretty confident on the accuracy of my statement.

Now, beyond that general point, incentives and behaviors change.

When we are talking about insurances that provide services or solve issues directly for you, the harsh reality is that the insurance doesn't give a damn about your well being. They probably do care about you not switching companies so that they can continue to collect your premiums, but they won't go above and beyond to fix your issues. And depending on how the contracts and terms look like, there may be massive friction in dropping their service, so it can be the case that customers will put up with the shittiest of services for a long time. Coming back to story number one, my friend's landlord hasn't switched companies after that whole mess.

When it comes to money-paying insurances, they obviously have an incentive to pay as little as possible. But I find those agreements to be less susceptible to trickery and frustrating situations, due to paying money being a much less arguable subject. It's easy for the insurance company in story #1 to say they are fulfilling their duties and shift blame on the technical complexity of the leakage issue. On the other hand, a life insurance can't fuck around much. If the guy is dead, is dead, and they have either paid the agreed upon sum or they haven't. There isn't much room for covering bases in crappy ways.

And then, looking at the division by small money sum/large money sum in the case of the bad event, I think there's a pretty ugly reality that you don't find in textbooks but do face in the trenches when it comes to small money sum insurance. What's the simplest way to save money for them? Well, as silly as it sounds, it might be to simply not do their part. Picture this: you have hired a travel insurance, which should pay if your airline loses your luggage. No big deal, maybe they only cover up to 500$. That happens, and you get in touch, but they fuck around with red tape and questions and delays and not answering the phone, and a month and two pass and you don't get the 500$ reimbursed. What are you going to do about it? I know something, you are most probably not going to sue them. It's not worth doing it given how much you'll have to pay in lawyers. It could even be that the terms you agreed included that legal matters should be solved in a different country that the one you live in.

When it comes to large money sum insurances, I feel things look better. If your partner dies and their life insurance doesn't pay you the 150K$ they should, I'm pretty confident you are going to go after them in court (and hopefully, the chances of succeeding should be high).

Now, my final conclusion after all of this bit on game theory and types of insurances rant is that:

- Small-money-sum, service-delivering insurance looks terrible for you as the customer.

- Large-money-sum, money-delivering insurance looks like a more interesting option.

And then there's Bitcoin

The alternative to buying insurance is not doing so. This means you take the risk of shit hitting the fan, but you keep your premium money in your pocket. And important part of the decision making, thus, is what the hell will you do with your money.

Conventional wisdom here is simple: you put your dollars in a piggy bank, and keep it safe so that when your boiler breaks down, or you crash your car, or you get diagnose with diabetes, you can use your savings to deal with the problem. But we all know that keeping fiat in the piggy, or a bank, is a stupid thing to do in this fiat world of ours. It will get inflated away and be worth nothing eventually.

Then Bitcoin comes into the scene. This changes things completely our options. With Bitcoin, the piggy bank gets a boost. Things make sense again, because you can properly store your funds there and they will be waiting for you when bad luck knocks at your door. And actually, if you get lucky and bad luck doesn't knock for some time, your bitcoin will keep compounding and possibly grow much more in fiat terms.

You can also look at the same idea the other way around: spending your money on the insurance comes with missing out the fiat gains that the equivalent bitcoin amount would have provided you with.

Decision making model, revisited

Earlier, I presented the first simple and naive insurance cost vs bad event cost model. But my previous side-rants should have made it obvious that such a model is not accurate at all because it doesn't contemplate:

- The risk of the insurance company not doing their part, partially or completely.

- The chances of recovering from the previous situation through court.

- The fact that you can save the premium money into Bitcoin, a modern era novelty that raises the opportunity cost of paying premiums through the roof.

Taking these into account, I've personally thought long and hard and I feel like I've settled for the following decision making process:

- If the cost of dealing with some insurable bad event is below 10,000€, do not buy any insurance. DCA the premiums into Bitcoin instead and use that piggy bank for the rainy day should it ever come.

- If the cost is above 10,000€, look for money-paying insurance options. Avoid service-delivering insurance.

- If there are money-paying options, judge them with the naive model:

- Compute how much you'll pay in premiums (insurance cost) while applying whatever CAGR you expect for Bitcoin, for the next 10 years.

- Multiply the chances of the insurable bad event happening times the expected cost of it (bad event cost), for the next 10 years.

- The insurance makes sense if:

- Bad event cost is higher than insurance cost

- Or bad event cost is higher than all your savings and accessible debt, which means facing it could wreck your life

- Again, if you don't buy the insurance, DCA the premiums into Bitcoin instead and use that piggy bank for the rainy day should it ever come.

I'm hoping this made sense. If you have personal opinions or interesting experiences with insurance, I would be happy to hear your thoughts. Criticism is also very welcome. As always, thanks for reading and I'll see you next month.

Previous episodes

- Episode 1: #47539

- Episode 2: #61708

- Episode 3: #71794

- Episode 4: #83670

- Episode 5: #98216

- Episode 6: #111818

- Episode 7: #124601

- Episode 8: #140816

- Episode 9: #154229

- Episode 10: #168432

- Episode 11: #181336

- Episode 12: #197688

- Episode 13: #212587

- Episode 14: #249798

- Episode 15: #265819

- Episode 16: #288719

- Episode 17: #322189

- Episode 18: #363765

- Episode 19: #394704

- Episode 20: #450792

- Episode 21: #476945

- Episode 22: #522161

- Episode 23: #550749

- Episode 24: #583121

- Episode 25: #622095

- Episode 26: #660530

Footnotes